[ad_1]

Get the free Morning Headlines electronic mail for information from our reporters internationally

Sign as much as our free Morning Headlines electronic mail

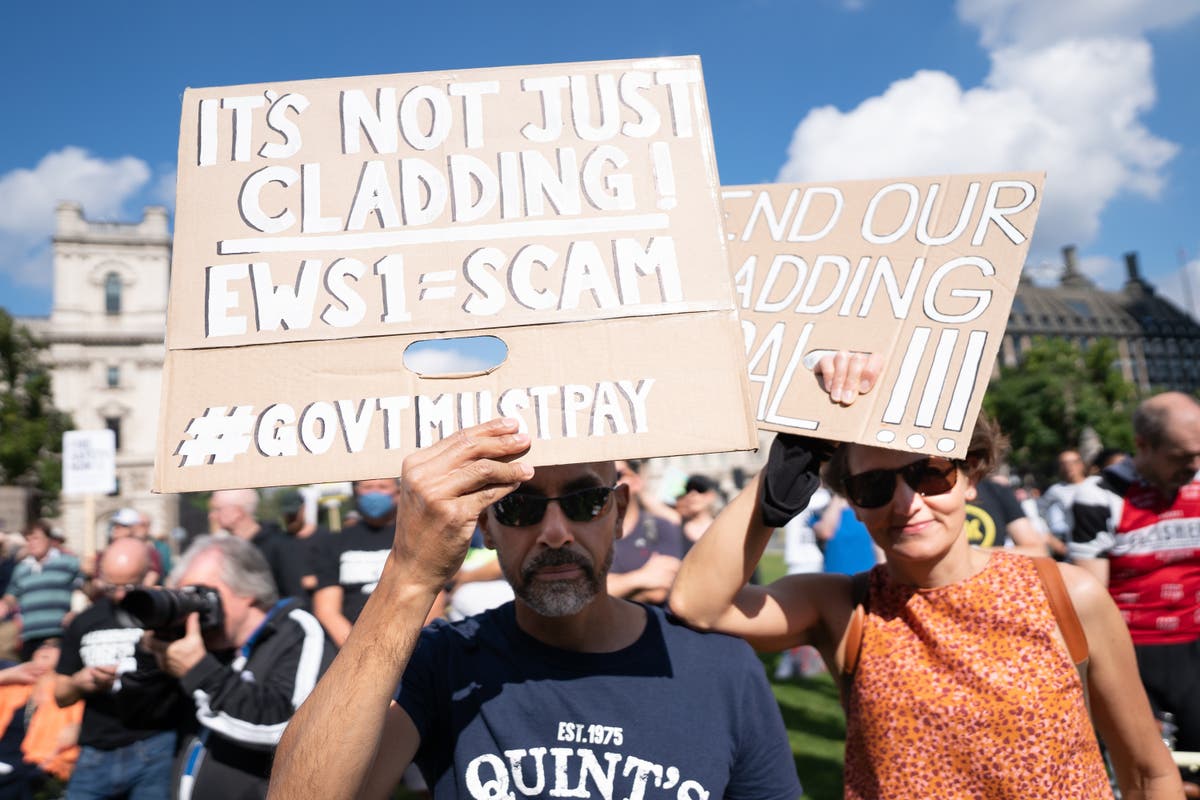

Thousands of residents trapped in properties with Grenfell-style cladding that they can’t promote are being “scammed” by insurers demanding unaffordable premiums regardless of being advised the buildings are secure, The Independent can reveal.

Nearly seven years after the tragedy, which happened in west London in June 2017, residents residing in cladded properties are seeing their insurance coverage prices surge by as much as 1,000 per cent.

One lady, whose one-bed flat the place she lives with her child was declared secure, noticed her annual insurance coverage invoice soar from £247 to £2,626 in simply two years – a tenfold improve. She advised The Independent: “How far does this go before I literally can’t beg, borrow, pay it back? The sky’s the limit if no one else will touch us.”

Have you been affected by this? Email andy.gregory@unbiased.co.uk

Campaigners and politicians have condemned the scenario, with Labour claiming that harmless leaseholders are being “scammed” by “exorbitant insurance costs”.

The Grenfell Tower hearth, which unfold from a defective fridge on the fourth flooring and quickly engulfed the whole constructing, threw the difficulty of cladding into the highlight, with 230,000 properties throughout the nation subsequently recognized as being lined in equally harmful materials.

Tens of 1000’s of properties have since been deemed secure or stripped of the fabric. But insurance coverage corporations prepared to insure these buildings have been accused of profiteering from the difficulty, whereas big-name insurers keep on the sidelines – mountain climbing up costs.

Stella Williams, whose insurance coverage invoice has soared by 1,000 per cent, with her daughter

(Stella Williams)

The authorities is now being urged to financially again a long-awaited scheme, arrange by the insurance coverage trade, to attempt to lower prices. But critics say it’s unlikely to make a lot distinction as solely a handful of insurers are collaborating – and solely then to assist present clients.

Labour MP Barry Gardiner advised The Independent: “Leaseholders are being scammed once again. Why should innocent leaseholders trapped in high-rise blocks with fire safety defects have to pay out for the exorbitant insurance costs?

“These are a direct result of the negligence and incompetence of the development and construction sectors.”

As effectively as properties clad with flammable supplies being pricey – or not possible – to insure, properties the place cladding has been judged to satisfy the brand new PAS 9980 security commonplace are additionally going through skyrocketing premiums. Insurers insist they nonetheless have to cost extra as a result of the federal government measure of threat to life doesn’t replicate the danger to the buildings themselves.

Stella Williams, who lives in a one-bed leasehold flat in Borehamwood, Hertfordshire, with her 11-month-old daughter, noticed her annual insurance coverage invoice greater than triple from £247 in July 2021 to £848 the next yr.

Despite a report discovering two months later that her five-storey constructing’s cladding met the federal government security commonplace, figuring out solely the timber balconies as requiring remediation, Ms Williams’s insurance coverage premium has now soared to an annual charge of £2,626.

Property managers FirstPort advised her this supply – which features a £10,000 extra for all dangers, even a leak, rising to £100,000 for hearth – was the one one they obtained for the 2 36-flat blocks after approaching 22 insurance coverage corporations, at the very least eight of whom straight cited cladding when declining to make a proposal.

“It’s now taking over my life – it’s just the fear of ‘what’s going to happen?’,” Ms Williams, a scientist who works in blood issues, advised The Independent. “What happens when we get a new bill in October?”

Seventy-two folks died in the Grenfell hearth, which broke out in west London in June 2017

(Steve Parsons/PA)

“I just feel really trapped,” mentioned Ms Williams, aged 40, who bought the one-bed flat utilizing Help to Buy in 2016. “It does affect you – I want to be happy around my baby, I don’t want her to grow up with stress around her. But it’s really difficult.”

Questioning why the federal government’s commonplace of remediation will not be ok for insurers, Ms Williams mentioned: “If the government really believe the risk is so low, then why can’t they underwrite my property?”

Ms Williams is way from alone in urging ministers to intervene, with the Association of British Insurers (ABI) itself amongst these calling for the federal government to again its new scheme.

When he was communities secretary in 2022, Michael Gove requested the City watchdog, the Financial Conduct Authority, to look into excessive insurance coverage prices for flats. The FCA mentioned in a report later that yr that it discovered proof of “some high commission rates” and that the availability of insurance coverage had “contracted significantly”.

‘Too little, too late’

The ABI hopes insurance coverage corporations will use the brand new Fire Safety Reinsurance Facility to assist shoulder the danger and convey prices down, mentioned Mervyn Skeet, the ABI’s director of common insurance coverage. But he was unable to say how a lot premiums may very well be decreased by.

Currently, simply Allianz, Aviva, Axa, RSA and Zurich have agreed to the scheme, and solely to reinsure present clients who’re nonetheless awaiting remediation works – a mere fraction of these doubtlessly going through hovering payments.

Of the 230,000 properties with unsafe cladding in buildings taller than 11m, work has already been accomplished in 55,000 of those – that means they won’t be eligible for the scheme.

Ms Williams bought one of many 72 flats in her twin block in Hertfordshire in 2016

(Stella Williams)

“It’s too little, too late – still no one can tell us how many people are going to be helped and what ‘good’ will look like. Too many people are ruled out of help,” mentioned Giles Grover, of End Our Cladding Scandal, whose personal premium continues to be up 400 per cent, even after three years of labor to switch the dangerous cladding at a value of £12m.

“Unfortunately, the government is resisting all calls to intervene. They’re still relying upon industry to turn around and stop ripping us off.

“It’s vital the Treasury agrees to back this scheme, otherwise [insurers] are continuing to profiteer from innocent leaseholders through the 12 per cent insurance premium tax.”

But Mr Skeet expressed hopes that ineligible buildings will nonetheless really feel the good thing about improved market competitors. The ABI additionally argues that authorities backing might additional increase market confidence and encourage extra companies to enroll.

He insisted his members have been “applying the proper rating to the risk they believe they’re taking on”, arguing that the post-Grenfell revelations of shortcomings in constructing laws had “significantly” elevated the dangers for insurers.

Mr Grover mentioned: “They say they’re not extorting us, they’re basing it on risk. Well what were you doing before? … You should have known. And if you didn’t know, you weren’t doing your due diligence.”

Martin Boyd, chair of the Leasehold Knowledge Partnership, added: “Insurance companies have done two things: put the premiums up, and the excesses too. I think that’s politely called double-dipping.”

Noting that “there is pretty obviously a correlation” between constructing resilience and life security, he pointed to figures displaying simply two of the 207 fire-related fatalities in residential properties over the yr to September 2023 have been high-rise buildings, regardless of firefighters responding to 707 blazes in these buildings.

“There is very little evidence – other than Grenfell – of big [fires in high-rises],” he mentioned, including: “If we want them to be as safe as modern buildings are built to now, then we need to demolish every single Georgian building in London, Bath, Edinburgh – wherever.”

A authorities spokesperson mentioned: “Many leaseholders in buildings with identified fire safety issues have suffered from high premiums for too long. We will monitor the Fire Safety Reinsurance Facility and work with insurers to improve understanding of building standards to ensure this new facility brings real change.

“We are working with insurers to improve understanding of building standards. Where buildings comply with the relevant standards, insurers should offer affordable premiums without requiring additional remedial works.”

[ad_2]

Source hyperlink